France’s former African colonies not only need to act in the light of France considering abandoning the Euro zone as the CFA is pegged to the Euro, but that the budgets of Francophone countries continue to be dictated by France

In recent weeks the French and international press have been full of stories about the resurgence of the Front National Party (‘FN’) in France led by Marine Le Pen. In the recent regional election in France at Brignoles, the party won with more than 54 percent of the vote. There is a trend towards the Right which has been sweeping across France and has become a leitmotif of political extremism across Europe.

In the run up to the European Parliament elections later this year the forces of the Right are edging out or threatening the traditional parties of power in France and across Europe. In a poll in mid-October 2013 in the respected weekly Le Nouvel Observateur, voters expressed their preference for the FN with 24 per cent of the vote, compared to 22 per cent for the conservatives and 19 per cent for the ruling Socialists. The FN has moved away from the fringes of the political party system to take up a place nearer to the centre. It has subsumed its appeal to racism, Holocaust denial and nativism under a cloak of anti-immigration policies coupled with a broad populist appeal against the demands of the European Union for austerity.

THE RISE OF THE RIGHT ACROSS EUROPE

This is a phenomenon growing wherever the austerity policies are viewed as inimical to social welfare. In Holland, the anti-immigrant Party for Freedom (‘PVV’) led by Geert Wilders, has had a similar success as the FN in France and leads in the opinion polls for the European elections. In Austria in September the anti-immigrant Austrian Freedom Party (‘FPO’) led by Heinz-Christian Strache won 20 per cent of the vote and almost stopped the ruling grand coalition of the two main centre-right and centre-left parties from getting a majority of the votes. In Britain the rise of the Eurosceptic party, the U.K. Independence Party (‘UKIP’) of Nigel Farage, which favours pulling out of the European Union altogether, is rising in the polls and claims to be the country's legitimate third party. UKIP swept the Liberal Democrats into fourth position as a national party and threatens to take votes from both Labour and the Conservatives at the European election and, perhaps, at the 2015 General Election.

Even in Germany, another Eurosceptic party, Alternative for Germany (‘AfD’) led by Bernd Lucke, Frauke Petry and Konrad Adam just missed out on a place in the Bundestag by a few tenths of a percentage point in last month's general election It did better than the Free Democrats (‘FDP’) which had formerly been in a coalition with Merkel. Elsewhere in Europe there has been a sharp rise in Eurosceptic parties as well as newly emboldened anti-immigrant and racist parties like Golden Dawn in Greece. There are similar neo-fascist groups in many European countries and they are joined by regional independence movements like Scotland, the Basques or Catalonia. The traditional two-party struggle between the parties of capital and labour are fraying at the edges as neither seem able or willing to deal with the problems of the lower and middle classes other than by increased austerity which compounds the distance between rulers and ruled. The Eurosceptic opposition parties have morphed into anti-Euro, anti-immigrant and nationalist parties with these issues as the foremost in their campaigns.

WILL FRANCE LEAVE THE EURO ZONE?

This bodes ill for Europe and its social and political cohesion. It also will have a dramatic impact on Africa if France leaves the Euro zone or if the increasingly dire financial crisis of the French banking system continues. In 2012 Professor Jacques Sapir wrote an important economic study (Jacques Sapir, Should we leave the euro?, Publisher Seuil, 12/01/2012, 204 pages) which was incorporated into the economic policy of the FN. This study advises that France, Italy, and Spain would all benefit from a Euro exit, restoring lost labour competitiveness at a stroke without years of depression. Their working assumption is that the Eurozone’s North-South imbalances have already gone beyond the point of no return. Attempts to reverse this by deflation and wage cuts must entail mass unemployment and loss of the industrial core. The answer is to pull out of the Euro, restore the national currencies and establish a flexible relationship among the currencies much as the old European currency ‘snake’ used to provide.

IMPLICATIONS OF LEAVING THE EURO ZONE FOR FRANCOPHONE STATES

Whether this is right or wrong is a moot question at the moment but the concept that France, among others, has the possibility of removing itself from the Euro is of great concern to francophone states, largely because the CFA francs, once pegged to the French franc, is now pegged to the Euro and indirectly linked to the fate of the French Central Bank.

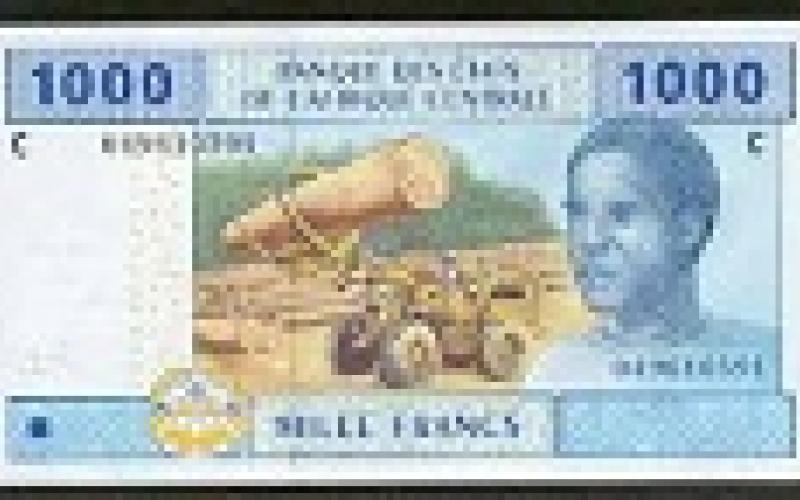

There are actually two separate CFA francs in circulation. The first is that of the West African Economic and Monetary Union (WAEMU) which comprises eight West African countries (Benin, Burkina Faso, Guinea-Bissau, Ivory Coast, Mali, Niger, Senegal and Togo. The second is that of the Central African Economic and Monetary Community (CEMAC) which comprises six Central African countries (Cameroon, Central African Republic, Chad, Congo-Brazzaville, Equatorial Guinea and Gabon), This division corresponds to the pre-colonial AOF (Afrique Occidentale Française) and the AEF (Afrique Équatoriale Française), with the exception that Guinea-Bissau was formerly Portuguese and Equatorial Guinea Spanish).

Each of these two groups issues its own CFA franc. The WAEMU CFA franc is issued by the BCEAO (Banque Centrale des Etats de l’Afrique de l’Ouest) and the CEMAC CFA franc is issued by the BEAC (Banque des Etats de l’Afrique Centrale). These currencies were originally both pegged at 100 CFA for each French franc but, after France joined the European Community’s Euro zone at a fixed rate of 6.65957 French francs to one Euro, the CFA rate to the Euro was fixed at CFA 665,957 to each Euro, maintaining the 100 to 1 ratio. It is important to note that it is the responsibility of the French Treasury to guarantee the convertibility of the CFA to the Euro.

The monetary policy governing such a diverse aggregation of countries is uncomplicated because it is, in fact, operated by the French Treasury, without reference to the central fiscal authorities of any of the WAEMU or the CEMAC states . Under the terms of the agreement which set up these banks and the CFA the Central Bank of each African country is obliged to keep at least 65% of its foreign exchange reserves in an “operations account” held at the French Treasury, as well as another 20 percent to cover financial liabilities.

The CFA central banks also impose a cap on credit extended to each member country equivalent to 20 percent of that country’s public revenue in the preceding year. Even though the BEAC and the BCEAO have an overdraft facility with the French Treasury, the drawdowns on those overdraft facilities are subject to the consent of the French Treasury. The final say is that of the French Treasury which has invested the foreign reserves of the African countries in its own name on the Paris Bourse in Euros.

FRENCH CONTROL OF AFRICAN ECONOMIES

In short, more than 80 percent of the foreign reserves of these African countries are deposited in the ‘operations accounts’ controlled by the French Treasury. The two CFA banks are African in name, but have no monetary policies of their own. The countries themselves do not know, nor are they told, how much of the pool of foreign reserves held by the French Treasury belongs to them as a group or individually. The earnings of the investment of these funds in the French Treasury pool are supposed to be added to the pool but no accounting is given to either the banks or the countries of the details of any such changes. The limited group of high officials in the French Treasury who have knowledge of the amounts in the “operations accounts”, where these funds are invested; whether there is a profit on these investments; are prohibited from disclosing any of this information to the CFA banks or the central banks of the African states.

The problem is that the French have hypothecated via the French Treasury much of the African reserves held in the name of the Treasury. France has run out of money. It has massive public and bank debt. It has the largest exposure to both Greek and Italian debt (among others) and has embarked upon yet another austerity plan. Its credit rating is at risk again and the upcoming stress tests on the European banks by the ECB will show serious and risky undercapitalisation among the French banks. It vast expenditures in pursuing its wars in Libya, Mali and the Central African Republic have exhausted most of the its defence budget. The reason it has been able to sustain itself so far is because it has had the cushion of the cash deposited with the French Treasury by the African states since 1960. Much of this is held in both stocks in the name of the French Treasury and in bonds whose values have been offset and used to collateralise a substantial amount of French gilts

FRANCOPHONE STATES NEED TO WAKE UP

The francophone African states are only reluctantly becoming aware that they may never see their accumulated assets again as these have been pledged by the French Treasury against the French contribution to the several European bailouts. French Treasury officials reckon that if France changes it relationship to the Euro it will have the effect of releasing around 40 percent of the French debt exposure and will extend a lifeline to the French Treasury. It has not calculated what will happen to the CFA francs.

However, a change in France’s relations with the Euro will have a devastating effect on francophone Africa whose currencies are pegged to the Euro and notionally supported by the French who may be planning on leaving the Euro. It is not surprising that the FN and the other nationalist or Eurosceptic parties of Europe have paid no attention to the consequences for Africa of a “Frexit”. With a core of racist, anti-immigrant ideologies at their core they spend very little of their time worrying about Africa. The French Government has a direct responsibility for this but will only act if the forces of francophone Africa force such a discussion.

The cosy system of françafrique which keeps African presidents happy and wealthy and which rewards French companies and political parties for their efforts to keep African Presidential coteries rich will not survive such a wrench. It is up to the francophone Africans to demand from their leaders that they act to preserve whatever is left of the currency reserves in France and start making plans for the collapse of the Euro.

* Gary K. Busch (Dr)

* THE VIEWS OF THE ABOVE ARTICLE ARE THOSE OF THE AUTHOR/S AND DO NOT NECESSARILY REFLECT THE VIEWS OF THE PAMBAZUKA NEWS EDITORIAL TEAM

* BROUGHT TO YOU BY PAMBAZUKA NEWS

* Please do not take Pambazuka for granted! Become a Friend of Pambazuka and make a donation NOW to help keep Pambazuka FREE and INDEPENDENT!

* Please send comments to editor[at]pambazuka[dot]org or comment online at Pambazuka News.

- Log in to post comments

- 3799 reads

Author

Anonymous (not verified)