‘Africa Rising’ in retreat: Signs of new resistances

Capitalism is bleeding Africa to death: illegal financial flows, legal financial outflows, FDI flows, foreign indebtedness, sub-imperial accumulation, new subsidies for infrastructure financing and uncompensated mineral and oil and gas depletion. The continent is further threatened by land grabs, militarization and climate change. Only rising social resistance can halt and reverse these trends.

At the very moment that Africa’s GDP ceased its rapid 2002–11 increase, a profound myth took hold in elite economic and political circles, embodied in the slogan “Africa Rising.”[1] That myth persists. Deutsche Bundesbank president Jens Weidmann claimed in June 2017 at a Berlin conference, “Africa stands ready to benefit from an open world economy. Its economic outlook is positive.”[2] The conference was arranged by German finance minister Wolfgang Schäuble to promote his G20 “Compact with Africa,” whose “main aim is to lower the level of risk for private investments” (but in the run-up to the German election, he and Angela Merkel were obviously also concerned to give the impression the strategy would reduce Europe’s African refugee crisis).[3]

In reality, after the 2011 peak of the commodity super-cycle and subsequent price crash, it was simply illogical to proclaim that Africa was prospering in “an open world economy”, given that so many of the continent’s economies depend on mineral and oil deposits whose extraction is dominated by transnational corporations (TNCs) and whose prices have been on a roller-coaster since 2002. A brief commodity price recovery in 2016 and ongoing drop in the value of most African currencies did not set the stage for renewed competitiveness, business confidence, or TNC investment, but instead catalyzed another round of fiscal crises, extreme current account deficits, sovereign debt defaults and intense social protests.

There is no hope of a decisive upturn on the horizon, despite hype surrounding China’s “One Belt, One Road” (OBOR) mega-infrastructure projects, touted for restoring some market demand for construction-related commodities.[4] As Xin Zhang explained, “Although there is an element of US-China competition for global hegemony behind the OBOR, the main driving force is the pressure from ‘over-accumulation’ in a typical capitalist economy when it approaches the end of a major cycle of capitalist cyclic change…. However, in China, there is also an ongoing debate about whether it is economically rational to pour such huge amounts of money into low-return projects and high-risk countries, especially in the case of massive infrastructural projects.”[5] The largest of China’s “Maritime Silk Road” enterprises reaching into Africa was Tanzania’s $11 billion Bagamoyo port, planned in 2013 to handle ten times more containers than nearby Dar Es Salaam harbor. The project, Forbes observed, was “vying to become the largest port in Africa upon completion,” but was cancelled in 2016 due—according to Deloitte and Touche—“to austerity measures introduced in Tanzania in order to reduce the widening budget deficit.”[6]

At the same time in Durban, the $20 billion expansion of the continent’s current main container port (which had also aimed at increasing containers 8-fold to 20 million per annum by 2040) was delayed until at least 2032. Corruption in lending and locomotive acquisition (both from China) implicating the South African parastatal Transnet is one factor; rising social resistance to port expansion is another; but the overarching problem was the post-2011 collapse of the Baltic Dry Index, signifying a profound crisis across world shipping.[7]

Although the $5 billion Lamu port construction in Kenya now underway not far from the Somalia border will link to South Sudan’s oil fields, between civil war there and Al-Shabaab’s attacks on Kenya (including kidnapping of a top official when she was unveiling Lamu’s spatial plan in July), the project is extremely risky, and 2017 also witnessed widespread community protest, including against a $2 billion coal fired power plant at the port, on grounds of climate change.[8]

Although a $3.2 billion Nairobi-Mombasa rail line was recently built and a $3.6 billion Uganda-Tanzania oil pipeline is planned, and although Ethiopian sweat-shop manufacturing is booming and can now be exported directly via n a $4 billion Addis Ababa-Djibouti railroad, all with Chinese aid, the downturn halved the value of East Africa’s large infrastructure projects under construction last year.

Southern Africa also faced a 22 percent fall in project numbers (to 85 in 2016), down from a cumulative $140 billion in 2015 to $93 billion in 2016, Deloitte also reported. Other recent mega-project reversals associated with Chinese over-reach or outright failure, according to the Wall Street Journal, include cancelled railway initiatives in Nigeria ($7.5 billion) and Libya ($4.2 billion), petroleum expansion in Angola ($3.4 billion) and Nigeria ($1.4 billion), an irreparably damaged coal-fired powerplant in Botswana ($1 billion), and metal smelting investments in the DRC and Ghana ($3 billion each).[9] The world’s largest dam, the $100 billion Inga Hydropower Project on the Congo River (three times the size of China’s Three Gorges), is also on indefinite hold after the World Bank pulled out last year and after Obama Administration officials rejected Beijing’s 2014 appeals for a joint venture.

The crisis of the extractive industries is also witnessed in the plummeting share prices of most mining houses, by more than 75 percent from their early 2015 levels, led by those with African exposure. Neither the entry of the Brazil-Russia-India-China-South Africa (BRICS)[10] bloc nor the G20’s meager new aid promises—mainly aimed at subsidizing TNCs—can disguise the generalized stagnation within the circuits of the world economy most important to Africa or indeed to global prosperity and ecological sanity.[11]

Even before the 2011 commodity peak and 2015 crash, the neoliberal export-oriented strategy had done enormous damage to human development, gender equity, and the natural environment.[12] Although rates of poverty, mortality and morbidity, and education have improved somewhat (especially after the West’s G7 debt relief package in 2005 which allowed the phase-out of what had been prohibitive user fees for basic state services), the conditions for reproduction of daily life in Africa have not, especially since the onset of global recession in 2008.[13]

Africa’s per-capita GDP levels did indeed rise rapidly from 1998 until then, but with very little trickling down. In 2013, the African Development Bank’s chief economist, Mthuli Ncube, made the spurious claim that “one in three Africans is middle class.” In 2017, the bank reiterated that “one of the main drivers of the surge in consumer demand in Africa is the continent’s growing population (currently 1 billion) and expanding middle class (estimated at 350 million).” But Ncube had defined “middle class” as those who spend anywhere between $2 and $20 per day, with 20 percent in the $2–4 range and 13 percent from $4–$20. Both categories represent poverty incomes in most African cities, whose price levels make them among the world’s most expensive. The share of those spending above $20 per day was less than 5 percent and shrinking, Ncube’s own data revealed.[14]

A central reason for the disparity between official talk of “Africa Rising” and the deep poverty of most of the continent’s people is sheer looting: illicit financial flows (IFFs) as well as legal financial outflows in the form of profits repatriated to TNC headquarters. The most exploitative channels of foreign direct investment (FDI) tend to be those that come in search of raw materials. After the commodity crash, annual FDI inflows to Africa slowed by 15 percent from 2008 to 2016, but despite the reversal, the extractive industries’ existing pressures on people and environments intensified, as corporate desperation heightened site-specific industry malpractices, ecological degradation, social abuse, and labor exploitation. The metabolism of capital versus nature and society has amplified to the point even the mining houses’ Corporate Social Responsibility is in profound retreat.

That desperation was most obvious during 2015. The British mining firm Lonmin’s London listing plummeted from a high price of 427,800c per share in 2007 to just 41c in early 2016, mostly during late 2015 in a fall that was far faster and further than even in the wake of the firm’s 2012 massacre of 34 striking platinum mineworkers at Marikana, South Africa. The value of the Anglo American Corporation (a 1917 joint venture of Ernest Oppenheimer and JP Morgan), which for much of the twentieth century was the largest firm on the continent, shriveled by 93.6 percent from a 2008 peak (3540c per share) to a 2016 low (227c), prompting the company to slash mining employment by more than half and begin selling African assets to the Indian entrepreneur Anil Agarwal of Vedanta. Even the world’s largest commodity trading firm, Glencore (formerly owned by apartheid oil sanctions-buster Marc Rich and then by his protégé, the South African Ivan Glasenburg), fell 86 percent from its 2011 initial London listing price of 532c per share, to a low of 74c.

As shareholders demanded restoration of their wealth, such crisis conditions generated pressure for more intense extraction. In mid-2017, London-based Global Justice Now and several allies released a study by Mark Curtis estimating that forty-eight countries in Sub-Saharan Africa are “collectively net creditors to the rest of the world, to the tune of $41.3 billion in 2015.” According to Curtis:

African countries received $161.6 billion in 2015—mainly in loans, personal remittances and aid in the form of grants. Yet $203 billion was taken from Africa, either directly—mainly through corporations repatriating profits and by illegally moving money out of the continent—or by costs imposed by the rest of the world through climate change.

African countries receive around $19 billion in aid in the form of grants but over three times that much ($68 billion) is taken out in capital flight, mainly by multinational companies deliberately misreporting the value of their imports or exports to reduce tax.

While Africans receive $31 billion in personal remittances from overseas, multinational companies operating on the continent repatriate a similar amount ($32 billion) in profits to their home countries each year.

African governments received $32.8 billion in loans in 2015 but paid $18 billion in debt interest and principal payments, with the overall level of debt rising rapidly.

An estimated $29 billion a year is being stolen from Africa in illegal logging, fishing and the trade in wildlife/plants.[15]

As Curtis’s figures and the following pages show, regardless of whether Western or BRICS TNCs are to blame, the excessive profits exiting Africa take many forms. Below we consider IFFs, legal financial outflows, FDI flows, foreign indebtedness, South African sub-imperial accumulation, new subsidies used for infrastructure financing, and uncompensated mineral and oil and gas depletion. The continent is further threatened by land grabs, militarization, and climate change. Multilateral management like the Compact With Africa, Bretton Woods loans and United Nations climate finance aren’t helping; only rising social resistance can halt and reverse these trends.

Illicit Financial Flows

First, IFFs reflect many of the corrupt ways that wealth is withdrawn from Africa, mostly in the extractive sector. TNCs employ a myriad of crooked tactics in this regard, including mis-invoicing inputs, transfer pricing and other trading scams, tax avoidance and evasion of royalties, bribery, “round-tripping” investment through tax havens, and outright theft of profits. Examples abound: in South Africa, Sarah Bracking and Khadija Sharife reported that De Beers mis-invoiced $2.83 billion of diamonds over six years.[16] A report by the Alternative Information and Development Centre in Cape Town showed that Lonmin’s platinum operations have spirited hundreds of millions of dollars offshore to Bermuda since 2000.[17] And Vedanta chief executive Agarwal bragged at a Bangalore meeting that in 2006 he had spent $25 million to buy Zambia’s Konkola copper mines, Africa’s largest, and went on to reap at least $500 million profits from it annually, apparently through an accounting scam.[18]

Studies of IFFs by the Washington-based NGO Global Financial Integrity and by economist Leonce Ndikumana and his University of Massachusetts colleagues show how they have helped produce an Africa that is both “more integrated but more marginalized” in world trade. Ndikumana subsequently authored a 2016 UN Conference on Trade and Development (UNCTAD) critique of extractive industries, and his accounts of South African and Zambian operations provoked angry rebuttals from mining industry representatives who objected to the poor quality of statistics provided by the two countries’ governments. While this has required some recalculations, especially in copper and gold exports, the larger truth of these critiques of IFFs remains.[19]

There are also policy-oriented NGOs working against IFF across Africa and the South, including several with northern roots like Trust Africa’s “Stop the Bleeding” campaign, Global Financial Integrity (GFI), Tax Justice Network, Publish What You Pay and Eurodad. (A large share of the credit for making this a major African and world policy matter is due to GFI’s Raymond Baker, a U.S. businessman active in Nigeria before moving to the Brookings Institution where he began advocacy on the issue.) Localization has also occurred through NGOs which demand more accountability, including Trust Africa’s “Stop the Bleeding” campaign. Linking radical and liberal critiques of TNCs and African elites, the new-found visibility of IFFs gives hope to many who want Africa’s scarce revenues to be recirculated inside poor countries, not siphoned away to offshore financial centers. Nevertheless, the head offices of some NGOs remain wedded to the dubious theory that the bright light of transparency can uncover, disinfect and deter corruption. Their main task is to make capitalism “cleaner,” by bringing problems like IFFs to light.

Consider the case of Tanzanian NGOs, whose neo-colonial outlook was remarked upon by local Marxist scholar Issa Shivji more than a decade ago.[20] In June 2017, Tanzanian President John Magufuli demanded that Canadian mining giant Barrick Gold pay billions of dollars in taxes that had been illegally exported: “We are in an economic war,” he declared. “Billions in revenue have been lost. It’s something that is very painful and shameful for Tanzania.” In response, the NGO network HakiRasilimali—an affiliate of George Soros’ Publish What You Pay (PWYP)—praised Magufuli for standing up, but also warned the government to be mindful of the legal conundrums that could arise from “international legal commitments [under which] the government is bound with guaranteeing companies protection from nationalization and safeguards against retrospective legal applications.” The group further emphasized “the need to continue being an investor friendly country where both the investor and government engage in a win-win situation.”[21]

Such a mindset is not unusual in PWYP circuits. Still, to their credit, many NGOs, allied funders, and grassroots activists have put enough pressure on governments and corporations to compel the African Union and UN Economic Commission on Africa to at least commission an IFF study, led by former South African president Thabo Mbeki.[22] Published in mid-2015, his report used a conservative methodology to estimate that IFFs from Africa exceed $50 billion every year.

This IFF looting originates largely but not entirely in extractive industries. According to an even narrower accounting than Mbeki’s, the African Development Bank and allies’ African Economic Outlook report estimated $319 billion was robbed from 2001–10, with the most theft in metals, totaling $84 billion; oil, $79 billion; natural gas, $34 billion; minerals, $33 billion; petroleum and coal products, $20 billion; crops, $17 billion; food products, $17 billion; machinery, $17 billion; clothing, $14 billion; and iron and steel, $13 billion.[23] These data reaffirm the common charge that Africa is “resource cursed.”

From IFFs to LFFs

Even if IFFs were reduced, FDI would continue to impoverish African countries, in the form of Licit Financial Flows (LFFs). These are legal profits and dividends sent home to TNC headquarters after FDI begins to pay off. The payments of such outflows, along with interest and the net trading position, are termed the “current account.” According to the most recent International Monetary Fund Regional Economic Outlook, the last fifteen years or so have witnessed trade surpluses between Sub-Saharan African nations and the rest of the world reach 5.6 percent of GDP in 2011, followed by smaller net surpluses, and then in 2015-16, deficits of 3.1 and 2.0 percent of GDP, respectively, with more deficits projected by the IMF.[24]

The current account measures not only the balance of imports and exports, but also the flows of profits, dividends, and interest. During the long commodity boom, Sub-Saharan Africa maintained a fair balance, and in 2004–08 even had an average surplus of 2.1 percent of GDP. But since 2011, it has plunged into the danger zone, with a current account deficit of 4.0 percent of GDP in 2016, led by Mozambique (–38 percent) the Republic of the Congo (–29 percent) and Liberia (–25 percent). Including North African countries, the full continent’s current account deficit was 6.5 percent of GDP in 2016, as a result of the fall in oil prices to a low of $26 per barrel in early 2016. Of fifty-four African countries, twenty had double-digit current account deficits in 2016. For context, the 1998 crash of leading East Asian economies was catalyzed by current account deficits of only 5 percent.

To cover a current account deficit, inflows of external finance are required. Such flows to Africa amounted to $178 billion in 2016, which was $5 billion less than 2015, largely as a result of a 60 percent decline in portfolio capital inflows (i.e., purchases of shares in debt or stock market investments, especially in the three major markets of Johannesburg, Cairo, and Lagos). Overseas development aid to Africa declined 2 percent in 2016, and remittances were virtually unchanged. Foreign Direct Investment is somewhat more complicated, however.

FDI in retreat

Third, partly due to the prolonged slump in commodity prices, the difficulty of raising new hard currency to pay profits and dividends rises as FDI falls. From a $66 billion peak annual inflow in 2008 to a 2016 level of $56 billion, FDI remains the second major inflow of hard currency to Africa, trailing only labor remittances. This is not only an African phenomenon: globally, annual FDI was $1.56 trillion in 2011, fell to $1.23 trillion in 2014, rose to $1.75 trillion in 2015, and then dipped to $1.52 trillion in 2016. As UNCTAD reported, 2016 “FDI flows to Africa continued to slide, reaching $59 billion, down 3 per cent from 2015, mostly reflecting low commodity prices.”[25] The anticipated 2017 uptick to $65 billion would still be less than 2014’s $71 billion.

The countries that saw the largest inflows of FDI in 2016 were the United States, with $385 billion; China (including Hong Kong), with $231 billion; and Britain, with $179 billion. Each outstrips Africa’s $59 billion. The single largest African FDI project in 2015–16 was an Egyptian property deal worth $20 billion, sponsored by the China Fortune Land Development company, but even this will create only about 3,000 jobs. Elsewhere in Africa in 2015–16, foreign investment funded only a few other mega-projects, including a Doha real estate development worth $8.5 billion, five Italian oil drill projects worth $8.1 billion, and a Chinese oil pipeline costing $6 billion.[26] Taken together, they suggest an extreme concentration of capital flows which will amplify Africa’s uneven development, following a pattern that anthropologist James Ferguson describes as “hopping and skipping” across the continent, instead of smoothly “flowing.”[27]

Curtis argues that inflows to Sub-Saharan Africa are far lower once both FDI outflows (such as the $11 billion from Angola alone in 2016) and corporate lending associated with FDI are subtracted. Hence in 2015, gross FDI in Sub-Saharan Africa totaled $41.2 billion, but outward FDI was $9.3 billion, leaving a net of $31.9 billion. Moreover, as Curtis shows, “figures from the World Bank suggest that 78 percent of private lending is FDI. This means there was $16.1 billion of loans. Removing this from $31.9 billion leaves $15.8 billion of FDI equity.” By comparison, Curtis estimates the entire set of capital inflows to Sub-Saharan Africa Curtis for 2015 at $162 billion, and the outflows at $203 billion (although natural capital accounting, discussed below, would show a far larger net deficit).[28]

The failure to sustain accumulation through FDI is due in part to shrinking commodities markets and the ebbing of the surge in Chinese fixed capital investment of 2009–12. UNCTAD also records “an overall increasing share of regulatory and restrictive policies in total investment policy measures over the last decade,” as a result of “a new realism about the economic and social costs of unregulated market forces”—although this may also be a symptom of “investment protectionism.”[29] The latter applies less in Africa, although South Africa has become more restrictive on trade as a result of deindustrialization (for example, by applying steel tariffs against Chinese dumping in 2015–17), and has cancelled some bilateral investment treaties because they conflict with the country’s Black Economic Empowerment policy.

Foreign debt explodes

The current account deficit in turn requires that state elites attract yet more FDI, so as to have hard currency on hand to pay back old FDI (usually as profit and dividend outflows), or if new investment is unavailable, as now appears the case, to take on new foreign borrowings. Because of these efforts to cover its payments deficits and slight trade deficit, Africa’s foreign debt is soaring. For Sub-Saharan Africa, what was a foreign debt in the $170–210 billion range from 1995 to 2005 (when G7 debt relief lowered it by 10 percent) has risen to nearly $400 billion by 2015.[30] Not only Chinese lending, but also a spate of Eurobonds became debilitating burdens in several countries, where by 2016 they represented a substantial share of the total public debt stock: 48 percent in Gabon; 32 percent in Namibia; 26 percent in Côte d’Ivoire; 24 percent in Zambia; 16 percent in Ghana; 15 percent in Senegal; and 13 percent in Rwanda.

The 2017 African Economic Outlook observed that “tighter financing conditions and increased debt financing have started to worsen debt service burdens, with an upward trend in both the debt-service-to-revenue ratio and the external debt-service-to-exports ratio.”[31] For petroleum-based economies, the report continued, there was a “a seven-fold increase in debt service, from an average of 8 percent of revenues in 2013 to 57 percent in 2016,” with Nigeria (at 66 percent) and Angola (60 percent) worst affected. Another fear is domestic debt, since the slowdown has also generated “a widespread increase in nonperforming loans, triggering higher provisioning, straining banks” profits, and weighing on solvency.”

In the case of the continent’s largest debtor, South Africa, foreign debt rose from $25 billion in 1995 to $35 billion in 2005, then soared to approximately $150 billion today, that is, doubling from 20 percent of GDP in 2005 to more than 40 percent now. The last time this ratio was reached was in 1985, with the result—thanks also to anti-apartheid sanctions–that South African president P. W. Botha defaulted on $13 billion in short-term debt and imposed exchange controls. The move signaled to the Anglophone capitalist class that the end of apartheid was near, and thus they should hasten to make favorable post-apartheid arrangements with the African National Congress, then in exile. Unfortunately, those arrangements entailed drawing South Africa much deeper into the world economy, and thus, as the current account deficit rose, deeper into foreign debt.[32]

Exploitation from within

A more nuanced account is needed of which firms are doing the looting. Western TNCs and governments have of course exploited Africa for centuries, and continue to do so. But Africa’s single biggest national source of FDI stock comes from within the continent, from South Africa. A dozen companies listed on the Johannesburg Stock Exchange draw steep levels of FDI profits: British American Tobacco, SAB Miller breweries (which in 2016 became a subsidiary of ABI, based in St. Louis), the MTN and Vodacom cellphone networks, Naspers newspapers, four banks (Standard, Barclays, Nedbank and FirstRand), the Sasol oil company, and the local residues of the Anglo American Corporation empire. Their profit rate drawn from South African assets has been 5 percent below the rate earned by the same firms in the larger region.[33]

The result is the systematic internal exploitation of the rest of Africa by South African capital, especially as the main retail chains—such as the Walmart-owned Massmart and its affiliates—use the larger market in the South to achieve production economies of scale that then overwhelm Africa’s residual basic-needs manufacturing sector. This too is a form of looting, also based on the IFF strategies used against South Africa by TNCs. Among others, South Africa’s MTN cellphone service was reported by the Amabhungane investigative journalist network to have Mauritian and Dubai financial offices which systematically skim profits for dubious tax-avoidance purposes from high-profit operations in Nigeria, Uganda and South Africa (corporate income tax rates in Mauritania are 3 percent, with no tax on capital gains).[34] This practice was most blatant under MTN chairperson Cyril Ramaphosa, who has been South Africa’s deputy president since 2014. Ramaphosa also held a 9 percent stake in Lonmin when similar sham “marketing” operations in Bermuda were used to fund tax avoidance.[35] A World Bank credit line worth in excess of $100 million, raised by Lonmin in 2007, was meant to sponsor the construction of more than 5,000 housing units, but only three were built—all under Ramaphosa’s direct responsibility.[36] When was fined $4 billion by Abuja authorities in November 2015 for failing to disconnect more than 5 million unregistered Nigerian customers during the state’s attempted crackdown on cellphone use by Boko Haram terrorists, the firm had few defenders. The fine was reduced to $1 billion only after South African President Jacob Zuma personally intervened during a 2016 state visit on MTN’s behalf.

Zuma has also stepped in militarily to defend the interests of South African capital. The oil operations of Zuma’s nephew Khulubuse in the Democratic Republic of the Congo were said to be worth $10 billion when the concession was acquired in 2010 (although there were unconfirmed reports he sold these interests). Not far away, 1,350 South African National Defence Force (SANDF) troops were stationed as part of a United Nations peacekeeping force (MONUSCO), but by early 2016, it became apparent that these troops were hardly keeping the peace, as a massacre occurred in their immediate vicinity.[37] Instead, as Belgian Royal Museum for Central Africa analyst Theodore Trefon explained: “Deployment of South African troops in the Intervention Brigade set up by the United Nations in March 2013 to reinforce MONUSCO in eastern DRC is an indication of President Zuma’s motivation to stabilize the region for economic reasons.”[38]

In a neighboring country to the north, the Central African Republic (CAR), the ANC’s “Chancellor House” investment arm sought a diamond monopoly in 2006, codified by Thabo Mbeki and CAR dictator Francois Bozizé. The latter was rejected by his former French sponsors a few years later and, facing a Chadian-backed uprising by the Seleka rebels, won military support from Pretoria. Justifying a five-year commitment to a military presence costing more than $100 million, South African deputy foreign minister Ebrahim Ebrahim explained, “We have assets there that need protection.”[39] But on March 25, 2013, more than a dozen corpses of South African soldiers were recovered in Bangui, after a two-day battle in which hundreds of local fighters and bystanders were killed. Two hundred SANDF troops were apparently trying to guard South African assets while Bozizé fled to safety. Seleka invaded his presidential compound, seizing power that day despite resistance from the SANDF men they labeled “mercenaries.” Two reporters for the Johannesburg Sunday Times reporters recorded the accounts of SANDF troops who made it back alive:

Our men were deployed to various parts of the city, protecting belongings of South Africans. They were the first to be attacked. Everyone thought it was those who were ambushed, but it was the guys outside the different buildings—the ones which belong to businesses in Jo’burg... We were lied to straight out... We were not supposed to be here. We did not come here to do this. We were told we were here to serve and protect, to ensure peace.[40]

Sometimes, when South African capital flows elsewhere in Africa, it carries the baggage of its nation of origin. When xenophobic unrest broke out in 2015, there were many branch plants of Johannesburg firms that became targets of protest by Nigerians, Zimbabweans, Malawians, Mozambicans, and Zambians concerned for their relatives’ safety. Hostility to Johannesburg capital is well-founded; in 2014 and 2016, its leadership was named the world’s most corrupt according to several key metrics (money-laundering, bribery and corruption, procurement fraud, asset misappropriation and cyber crime) compiled by PricewaterhouseCoopers.[41]

At the same time, since the late 1990s, South Africa’s current account deficit has soared, as nearly all of the country’s biggest companies have relocated to London or New York, taking their LFFs with them, including Anglo American and its historic partner De Beers, as well as SAB Miller, Investec bank, Old Mutual insurance, Didata IT, Mondi paper, Liberty Life insurance, Gencor (BHP Billiton), and a few others. As a result, in 2015, the South African Reserve Bank revealed that Johannesburg firms were in 2012–14 drawing only half as much in internationally sourced profits (“dividend receipts”) as TNCs were taking out of South Africa. But that was an improvement over the 2009–11 period, when local TNCs pulled in only a third of what foreigners took out.[42] One reason is that Johannesburg firms have been busier in the rest of Africa in the past few years, as mining, cellphones, banking, brewing, construction, tobacco, tourism, and other services from South Africa became more available up-continent.

Public subsidization and private financing

Another continual threat to the continent is ever more frenetic mining and petroleum extraction, notwithstanding falling prices, as a result of state subsidies. In 2017, the G20 proposed a Compact with Africa (CwA) to assure state support for so-called public-private partnerships across the continent, and to attract institutional investors with state guarantees. As leading financial analyst Helmut Reisen explained, given the anticipated asset base of “$100 trillion by 2020, institutional investors (pension, funds, life insurers and sovereign wealth funds) would need to invest one percent of their annual new inflows to fund Africa’s infrastructure gap, estimated at $50 billion per year.”[43] But according to the C20 group of civil society watchdogs, this strategy will translate into

higher costs for the citizens, worse service, secrecy, loss of democratic influence and financial risks for the public and the multinational corporations involved demand that their profits be repatriated in hard currency—even though the typical services contract entails local-currency expenditures and revenues—and that often raises African foreign debt levels, which are now at all-time highs again in many countries. The Compact also is silent regarding problems with (and popular resistance to) investor protection, such as the vague “fair and equitable treatment” clause in investment agreements and investor-to-state dispute settlement.[44]

The Harare-based African Forum and Network on Debt and Development and the Africa Development Interchange Network offered an even more stinging critique: “There is reason to fear that slavery and colonization may strongly come back. In any case, to use public money to protect private investment would equal to taunting the African populations. This can easily be understood only from the perspective of colonization or neoliberal exploitation. This is quite serious when we know that some African leaders hold fortunes outside their countries, to the benefit of Western banks.”[45]

Until the G20’s recent focus on just seven pro-Western African countries (Tunisia, Ethiopia, Morocco, Rwanda, Senegal, Ghana, and Côte d’Ivoire), it was generally assumed that the largest donor subsidies would go to the African Union’s Program for Infrastructure Development in Africa (PIDA). The continent-wide trillion-dollar PIDA is mainly aimed at extraction.[46] New roads, railroads, pipelines and bridges are planned, but they largely emanate from mines, oil and gas rigs, and plantations, and are mainly directed towards ports. Electricity generation is overwhelmingly biased towards projected mining and smelting needs, although the case of the parastatal mining firm Eskom, in South Africa is illustrative, as demand for its product fell at least 5 percent in late 2015, once adverse economic conditions forced mine shafts and foundries to close. In 2015, Eskom suffered regular brownouts, but after winter ended, a substantial surplus developed, leading the company to announce major coal-fired power station closures in 2017.

Subsidies of the sort envisaged in the CwA and PIDA could bring back the worst of FDI, especially from BRICS companies, such as the predatory South African firms mentioned above. Other companies with dubious records include Brazil’s Vale mining, responsible for mass displacement in Mozambique; Russia’s Rosatom, planning a proposed $100 billion nuclear reactor deal with Pretoria, as well as anticipated deals in several other African countries; India’s Vedanta, which has an extremely exploitative record in Zambia; and various Chinese parastatals and firms.[47] One channel through which they anticipate receiving indirect financing subsidies, in the form of loans at preferential rates, is the BRICS New Development Bank.[48]

The new wave of BRICS investment already appears to many in Africa as an intensified version of Western TNCs’ exploitative experiences, especially considering the pro-corporate arrangements contained in their Bilateral Investment Treaties with Africa.[49] There was initially hope expressed by commentators on the left—including Walden Bello, Horace Campbell and Radhika Desai—that the new BRICS financial institutions would break the Bretton Woods stranglehold.[50] Yet their arguments have not confronted such contradictions as their financing of destructive African energy and infrastructure projects, or their upholding of the dollar-centric Western monetary system, or the woefully inadequate climate change policies in which the BRICS are implicated. The BRICS $100 billion Contingent Reserve Arrangement, for example, requires any of the five member countries which fall into financial trouble (such as South Africa no doubt will be when its short-term foreign debt payments become unsustainable) to apply to the IMF for a structural adjustment loan and policy support once they have exhausted 30 percent of their borrowing quota, thus amplifying IMF leverage.[51] And the 2015 round of IMF shareholder restructuring gave substantial voting increases to China (up by 37 percent), Brazil (23 percent), India (11 percent) and Russia (8 percent), yet to accomplish this required that seven African countries lose more than a fifth of their IMF voting share: Nigeria (41 percent), Libya (39 percent), Morocco (27 percent), Gabon (26 percent), Algeria (26 percent), Namibia (26 percent) and even South Africa (21 percent).

Uncompensated natural capital depletion

Dependency-inducing financing arrangements and the continuation of FDI aimed mainly at extraction are responsible for Africa’s excessively rapid, poorly-compensated depletion of non-renewable resources. In Africa, this depletion occurs without the kinds of reinvestment that are more common in sites such as Norway, Australia and Canada, whose economies are also resource-based but not nearly so resource-cursed as Africa’s, in large part because they host the headquarters of mining and petroleum TNCs. Many BRICS corporations appear only too eager to continue this rapid depletion of Africa’s “natural capital,” as economists call natural resource endowments. Although the end of the commodity super-cycle will mean a lower rate of extraction measured in global price terms, this should not blind Africans to the continent’s residual colonial bias toward the removal of non-renewable minerals, oil, and gas, whose exploitation leaves Africa far poorer than anywhere else on earth.

That bias towards non-renewable resource depletion without reinvestment has caused the continent’s net wealth to fall rapidly since 2001. Even the World Bank admits that 88 percent of Sub-Saharan African countries suffered net negative wealth accumulation in 2010.[52] In absolute terms, the bank also acknowledges that this depletion of wealth amounted to 12 percent of the sub-continent’s $1.36 trillion GDP in 2010 alone, i.e. $163 billion (and far more if the major North African oil-rich countries are included).

Estimates of the depletion of Africa’s wealth should be part of every critique of “extractivism,” to make the case that until countries achieve local control of their own resources, minerals and oil should be left in the soil. (For example, grassroots activists critical of diamond extraction in eastern Zimbabwe, oil in Nigeria, and coal, platinum, and titanium in South Africa regularly insist on leaving resources in the ground.) For oil, the compensation due from the North—as a down-payment on “climate debt” owed Africa—simply on grounds of climate change mitigation would be substantial. Such a strategy was attempted in the Ecuadoran Yasuni National Park, and while it did not succeed in the short run (2007–13), it deserves to be revitalized, as a means of compensating historically-exploited fossil fuel-rich countries.

Land grabs, climate change and militarization

Finally, contemporary African political economy and ecology are characterized by a trio of destructive phenomena: land grabs, militarization, and climate change. The most immediate threats face the African peasantry, especially women, and especially those in areas attractive to foreign investors. Already, small farmers are being displaced in Ethiopia, Mozambique, and elsewhere as a result of land grabs by Middle Eastern countries, India, South Africa, and China.[53] The growing role of the U.S. military’s Africa Command in dozens of African countries attests to Washington’s overlapping desire to maintain control amid rising Islamic fundamentalism, from the Sahel to Kenya—which are, coincidentally, theaters of war in the vicinity of large petroleum reserves.[54]

Climate change will affect the most vulnerable Africans in the poorest countries, who already suffer extreme stress from war and displacement in West Africa, the Great Lakes, and the Horn of Africa. Although Clionadh Raleigh of the Armed Conflict Location Events Data (ACLED) project at Sussex University argues that climate change does not directly cause protests and social unrest, in part because of the role mutual aid systems, there is nevertheless no doubt that worsening agricultural conditions accelerate migration to urban areas, which in turn puts more strain on the social fabric of Africa’s cities.[55] At the same time, the further application of neoliberal state-shrinking public policy is bound to generate yet more social stress, as was the case in Syria prior to the 2011 uprising.

Rising social resistance

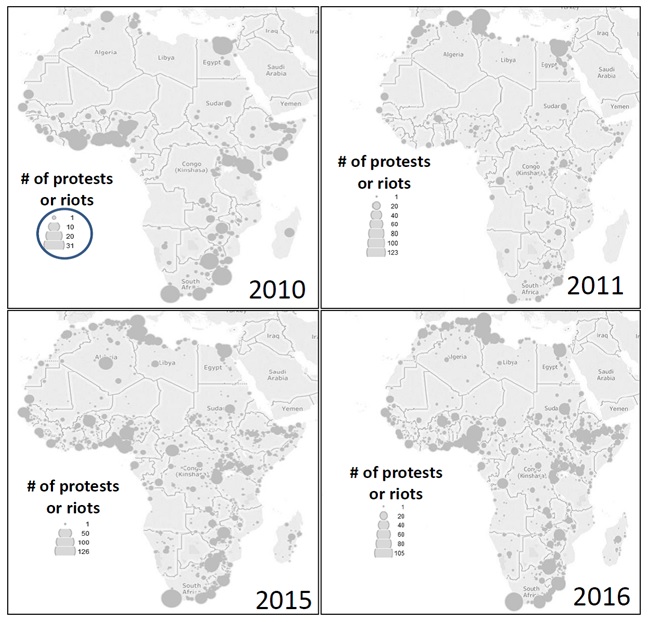

Largely because of these worsening socioeconomic conditions, African activists and “uncivil society” groups—that is, those willing to express frustration by means other than what are often termed the “invited spaces” of official participation—have been protesting and resisting at rising rates across the continent. There are various ways to measure this power, including police statistics, journalistic accounts, and business executive surveys. According to research by scholars at the universities of Sussex and Texas, protest incidents rose dramatically in 2010–11 and have stayed at remarkably high levels in many African cities.[56]

In 2010, the Armed Conflict Location and Event Data database recorded scores of protests (especially those that turned violent, typically facing police repression) in Cairo and Alexandria, Mogadishu, Nairobi, the cities and towns on the Gulf of Guinea—especially in Nigeria—and in the four largest South African cities: Johannesburg-Pretoria, Cape Town, Durban, and Port Elizabeth. In 2011, dozens of protests broke out in these cities. Tunis, Algiers and Cairo were measured as hosting more than one hundred protests each.

In 2015–16, the continent witnessed even more intense protests across North Africa, Nigeria, and South Africa. In addition, Southern Africa witnessed high levels of resistance in Harare, Kinshasa, and Goma, in the Democratic Republic of the Congo, as well as in Zambia and Madagascar, where the capitals of Lusaka and Antananarivo recording substantial increases compared to 2011. East Africa and the Horn witnessed scores of protests in Nairobi; Kampala; Bujumbura; Khartoum, and Addis Ababa and surrounding towns. West African protests were led by Nigerians, but there were many other scattered sites of unrest in the Gulf of Guinea. 2016 saw new rounds of protests in North Africa, most in the major 2011 sites: Tunisia, Egypt, Libya, and Algeria. Although the counter-revolution had since prevailed in most of these countries, the activists were not deterred from expressing grievances. State repression has accordingly intensified in many countries as a response to the protest upsurge.[57]

The African Development Bank, the World Bank, and the Organization for Economic Cooperation and Development also measure protests with data based upon Reuters and Agence France Press reports, and in 2017 observed that higher wages and better working conditions consistently ranked as the main motives for protests in recent years.[58] A good share of the turmoil in Africa prior to the 2011 upsurge took place near sites of mineral wealth.[59] Subsequently socioeconomic protests included the famed Tunisian revolt in 2011 catalyzed by Mohamed Bouazizi’s self-immolation. Both Tunisia and Egypt generated such intense revolutionary bursts of energy because their independent labor movements were also ascendant. Notwithstanding extreme unevenness across and within the continent’s trade unions, Africa is ripe for a renewed focus on class struggle.

Indeed, as socioeconomic conditions continue to deteriorate, the World Economic Forum’s Global Competitiveness Report—an annual survey of 14,000 business executives in 138 countries —has ranked the continent’s workers as the least cooperative on earth. In 2016, workforces from South Africa (ranked as the world’s most militant every year since 2012), Chad, Tunisia, Liberia, Mozambique, Morocco, Lesotho, Ethiopia, Tanzania, Algeria, and Burundi were among the top twenty-five most confrontational proletariats.[60] (Meanwhile, the most cooperative workers are in Norway, Switzerland, Singapore, Denmark, and Sweden.)

With GDP growth declining to just 1.4 percent in 2016 and commodity prices still low, and with declining levels of transnational corporate investment seeking desperately to exploit the continent, Africa’s current contradictions may well spark more socio-political explosions. The idea of a Polanyian “double movement”—i.e., social resistance against marketization– has long applied to Africa. IMF austerity and subsequent riots spread across the continent during the 1980s, and to some extent catalyzed democratization movements during the early 1990s, but mainly failed to establish durable liberal political regimes. With the spoils of exuberant commodity markets accruing to unaccountable elites, another intense protest wave began in 2011, sparked in North Africa by increasingly urgent economic grievances.[61]

However, an old problem arises. Frantz Fanon complained in Toward the African Revolution that “the deeper I enter into the cultures and the political circles, the surer I am that the great danger that threatens Africa is the absence of ideology.” In a speech titled “The Weapon of Theory,” Amilcar Cabral agreed: “The ideological deficiency within the national liberation movements, not to say the total lack of ideology—reflecting as this does an ignorance of the historical reality which these movements claim to transform—makes for one of the greatest weaknesses in our struggle against imperialism, if not the greatest weakness of all.”[62]

Samir Amin and other radical political economists have argued for an ideology and economic strategy of “delinking” since the 1960s. Today we might term such an effort the “globalization of people and de-globalization of capital,” a slogan that captures the soundest short-term economic strategy for what could become a post-FDI world, at a time the rates of growth of trade (especially shipping), FDI and North-South financial and aid flows are stagnant or even shrinking. It is high time that these arguments, long dismissed under the neoliberal ascendancy, be dusted off and put to work, to help Africans continue to rise against the chimera of “Africa Rising.” Those who would dispute this line of argument must confront evidence of the futility of Africa’s export-led economic fantasies, whether via the West or BRICS economies, three of which—South Africa, Brazil and Russia—have seen negative growth in 2016-17. And as a final clarion call for a radical reimagining of African political economy, there is also the political-ecological imperative to restructure the fossil fuel-addicted sectors of economy, as the world necessarily moves toward post-carbon systems.

Reversing the “Africa Rising” project, then, is the major challenge for Africans who rise up against injustice, especially in those forms in which they can build solidarity with the rest of the world’s oppressed peoples. For example, the struggle for AIDS medicines, once costing $10,000/year per person but now supplied free on a generic basis, was won since the early 2000s thanks to internationalist activism, and has raised life expectancy by more than a decade where applied. At this critical juncture, as the commodity super-cycle’s denouement now makes obvious the need for change, at least it is clear to all that Africans are not lying down.

* PATRICK BOND is professor of political economy at the University of the Witwatersrand, Johannesburg and author of Looting Africa (Zed Books, 2006). This essay was originally published by Monthly Review, September 2017.

Notes

[1] E.g., The Economist, “Africa Rising,” December 3, 2011; Alex Perry, “Africa Rising,” Time, December 3, 2012; Charles Robertson, “Why Africa will Rule the 21st Century,” African Business, January 7, 2013.

[2] Jens Weidmann, “Improving the Investment Climate in Africa,” Keynote speech at the Berlin conference, “G20-Africa Partnership: Investing in a Common Future" (June 13, 2017).

[3] Bundesministerium der Finanzen, “Compact with Africa”, G20 Finance Ministers Meeting, Baden Baden (March 30, 2017). The only African G20 member, South Africa, was fully assimilated into the program by the time of July’s conflict-ridden heads-of-state summit in Hamburg, in spite of beleaguered President Jacob Zuma’s regular anti-Western pronouncements. Neither Merkel, Zuma nor any others there could reverse U.S. President Trump’s threats to trade deals such as the Africa Growth and Opportunity Act, dramatic budget cuts to foreign aid (including food and medicines to Africa), or Trump’s intention to raise greenhouse gas emissions and discontinue United Nations Green Climate Fund payments.

[4] China suffers from the apparent exhaustion of prior sources of profitability, i.e., “an expanding external market, a relatively large reserve army of labor, and a low debt-income ratio,” according to Hao Qi (“Dynamics of the Rate of Surplus Value and the ‘New Normal’ of the Chinese Economy,” University of Massachusetts-Amherst Political Economy Research Institute Working Paper, June 22, 2017). The prior (2009-12) spatial fix of massive urban infrastructure and housing construction was also soon exhausted, leaving hundreds of Ghost Cities. The OBOR also appears as a potential $1 trillion mirage, and one that may in the process even crack the BRICS, in the event the Kashmir OBOR routing continues to cause extreme alienation between Xi Jinping and Narendra Modi, adding to severe new Sino-Indian military tensions at Bhutan’s Doka La Plateau border.

[5] Xin Zhang, “Chinese Capitalism and the New Silk Roads,” Aspen Review, 4, 2016.

[6] Wade Shepard, “These 8 Companies are Bringing the 'New Silk Road' to Life”, Forbes, March 12, 2017; Kennedy Kangethe, “East Africa Mega Projects Reduce by Half in 2016: Deloitte Report,” Capital Business, February 2, 2017.

[7] Patrick Bond, “Red-Green Alliance-Building against Durban’s Port-Petrochemical Complex Expansion,” in L.Horowitz and M.Watts (Eds), Grassroots Environmental Governance: Community Engagements with Industry (London: Routledge, 2017).

[8] Business Daily Africa, “Activists Demonstrate against Centum's Coal Project,” May 12, 2017. Courageous citizens’ groups facing police harassment as a result include Save Lamu, Cordio East Africa and Muslims for Human Rights.

[9] Wall Street Journal, “Beijing Shows More Caution on Africa Deals,” May 7, 2014.

[10] Bond and Ana Garcia (Eds) BRICS: An Anti-Capitalist Critique (Johannesburg: Jacana Media, 2015); Patrick Bond, “Can BRICS Re-open the ‘Gateway to Africa’?,” in C. Mutasa and D.Nagar (Eds), Africa and External Actors,(London: IB Tauris, 2017).

[11] David Harvey, Marx, Capital and the Madness of Economic Reason (London: Profile Books, 2017); Michael Roberts, The Long Depression (Chicago: Haymarket, 2016); Richard Walker (2016), “Value and Nature: Rethinking Capitalist Exploitation and Expansion,” Capitalism Nature Socialism.

[12] Samir Amin, Delinking (London: Zed Books, 1990); Patrick Bond, Looting Africa (London: Zed Books 2006).

[13] Vusi Gumede (Editor) The Great Recession and its Implications for Human Values: Lessons for Africa (Johannesburg: Real African Publishers, 2016).

[14] Mthuli Ncube,“The Middle of the Pyramid” (Tunis: African Development Bank, 2013); African Development Bank, OECD Development Centre, UN Development Programme and Economic Commission for Africa, African Economic Outlook (Tunis, 2017).

[15] Mark Curtis, Honest Accounts (London: Curtis Research, 2017).

[16] Sarah Bracking and Khadija Sharife, Rough and Polished (Manchester University: Leverhulme Centre for the Study of Value, 2014).

[17] Alternative Information and Development Centre, “Lonmin, the Marikana Massacre and the Bermuda Connection” (Cape Town: AIDC, 2014).

[18] Lusaka Times, “Video – Vedanta Boss Saying KCM makes $500 million Profit per Year,” May 13, 2014.

[19] Dev Kar and Josepth Spanjers, Illicit Financial Flows from Developing Countries: 2004-2013 (Washington, DC: Global Financial Integrity, 2015); Leonce Ndikumana, “Curtailing Capital Flight from Africa,” University of Massachusetts/Amherst Political Economy Research Institute, Amherst, June 2017; United Nations Conference on Trade and Development, Trade Misinvoicing in Primary Commodities in Developing Countries, Geneva, 2016.

[20] Issa Shivji,“The Silences in the NGO Discourse,” Africa Development, 31, 4, 2006.

[21] HakiRasilimali, “Position on Presidential Committees' Reports on Mineral Exports”, Dar es Salaam, June 16, 2017.

[22] Thabo Mbeki, Track it! Stop it! Get it! Illicit Financial Flow, Report of the High Level Panel on Illicit Financial Flows from Africa, United Nations Economic Commission on Africa, Addis Ababa, 2015.

[23] African Development Bank, OECD Development Centre, UN Development Programme and Economic Commission for Africa, African Economic Outlook 2013, Tunis, 2013.

[24] International Monetary Fund, Regional Economic Outlook: Africa, 2017, Washington DC, 2017.

[25] United Nations Conference on Trade and Development, World Investment Report 2017, Geneva, 2017.

[26] African Development Bank, OECD Development Centre, UN Development Programme and Economic Commission for Africa,African Economic Outlook 2017, Tunis, 2017,

[27] James Ferguson, Global Shadows: Africa in the Neoliberal World Order (Durham: Duke University Press, 2006).

[28] Curtis, Honest Accounts.

[29] United Nations Conference on Trade and Development,World Investment Report 2015, Geneva.

[30] IMF, Regional Economic Outlook: Africa, 2017.

[31] African Development Bank, et al, African Economic Outlook 2017.

[32] Patrick Bond, Against Global Apartheid (London: Zed Books, 2003).

[33] International Monetary Fund, “2016 Article IV Consultation: South Africa”, Washington DC, 2016.

[34] Amabhungane, “Ramaphosa and MTN’s Offshore Stash,” Mail&Guardian, October 8, 2015.

[35] Alternative Information and Development Centre, “Lonmin, the Marikana Massacre and the Bermuda Connection.”

[36] John Saul and Patrick Bond, South Africa’s Present as History: From Mrs Ples to Mandela and Marikana (Oxford: James Currey, 2014).

[37] Simon Allison, “South African Peacekeepers accused of Failing to Prevent DRC Massacre,” Daily Maverick, January 21, 2016.

[38] Theodore Trefon, “DRC in the Panana Papers,” Congo Masquerade, April 5, 2016.

[39] Khadija Patel, “SA Troops Killed in Central African Republic: Why, Mr President?,” Daily Maverick, March 23, 2013; Amabhungane, “Is This what our Soldiers Died For?,” Mail&Guardian, March 28, 2013.

[40] Graham Hosken and Isaac Mahlangu, “‘We were Killing Kids’,” Sunday Times, March 31, 2013.

[41] PricewaterhouseCoopers, “Global Economic Crime Survey,” Johannesburg, 2016.

[42] South African Reserve Bank, Quarterly Bulletin (June 2015), Pretoria, 2015.

[43] Helmut Reisen, “The G20 ‘Compact with Africa’ is Not for Africa’s Poor,” Berlin, Shifting Wealth, June 8 2017.

[44] C20, “The G20’s Compact with Africa,” Pambazuka, May 4, 2017.

[45] African Forum and Network on Debt and Development and the Africa Development Interchange Network, “The G20 Compact With Africa and the Germany Proposed Marshall Plan For Africa,” Harare, July 16, 2017.

[46] African Union, Programme for Infrastructure Development in Africa, Addis Ababa, 2012.

[47] Patrick Bond, “The BRICS Re-scramble Africa.” in R.Westra (Ed.), The Political Economy of Emerging Markets, (London: Routledge, 2017).

[48] Patrick Bond, “BRICS Banking and the Debate over Sub-Imperialism,” Third World Quarterly, 37, 4, April 2016.

[49] Ana Garcia, “BRICS Investment Agreements in Africa,” Studies in Political Economy, 98, 1, 2017.

[50] Walden Bello, “The BRICS: Challengers to the Global Status Quo.” Foreign Policy in Focus, August 29, 2014; Horace Campbell, “BRICS Bank Challenges the Exorbitant Privilege of the US Dollar,” TeleSUR, July 24, 2014; Radhika Desai, “The BRICS are Building a Challenge to Western Economic Supremacy,” Guardian, April 2, 2013.

[51] BRICS, “Treaty for the Establishment of a BRICS Contingent Reserve Arrangement,” Fortaleza, July 15, 2014.

[52] World Bank, Little Green Data Book 2014, Washington, DC, 2014; World Bank, The Changing Wealth of Nations, Washington, DC, 2011.

[53] Thomas Ferrando, “BRICS, BITs and Land Grabbing,” Paris, Sciences Po Law School, 2014.

[54] Nick Turse, “Africom Becomes a War-Fighting Combatant Command,” TomDispatch, April 13, 2014.

[55] Clionadh Raleigh, “Climate Violence?” Lecture to the Oxford Martin School, Oxford, May 11, 2017.

[56] ACLED, Armed Conflict Location Events Data, Sussex; Robert S. Strauss Center for International Security and Law, “Final Program Report on Climate Change and African Political Stability,” Austin, University of Texas, 2016.

[57] David Kode and M.Ben Garga, “Activism and the State,” Pambazuka, May 11, 2017.

[58] African Development Bank et al, African Economic Outlook 2017.

[59] Nicolas Berman, Mathieu Couttenier, Dominic Rohner and Mathias Thoenig, “This Mine is Mine! How Minerals Fuel Conflicts in Africa,” Oxford: Oxford Centre for the Analysis of Resource Rich Economies, 2014.

[60] World Economic Forum, Global Competitiveness Report, 2016-17, Davos, September 2016.

[61] Samir Amin, “An Arab Springtime?,” Monthly Review, June 2011; Rabah Arezki and Marcys Brückner,“Food Prices, Conflict, and Democratic Change,” University of Adelaide School of Economics Research Paper No. 2011-04, 2011; Jumoke Balogun, “Africa is Rising. Most Africans are Not,” Compare Afrique, February 15, 2013; John Beieler, “Protest Mapping,” State College, Penn State University, 2013; Ama Biney,“Is Africa Really Rrising?” Pambazuka, July 31, 2013; Adam Branch and Zachariah Mampilly, Africa Uprising: Popular Protest and Political Change (London: Zed Books, 2015); Sokari Ekine, “Defiant in the Face of Brutality: Uprisings in East and Southern Africa,” Pambazuka, 532, June 2, 2013.

[62] Frantz Fanon, Toward the African Revolution (New York: Monthly Review Press, 1967); Amilcar Cabral, “The Weapon of Theory,” Address to the first Tricontinental Conference of the Peoples of Asia, Africa and Latin America. Havana, January 1966.

major tour de force by

Ligação permanente

major tour de force by Patrick Bond. For more information on popular protest, social movements and class struggle in Africa over last few years see my project for the Review of African Political Economy (roape.net) on just that topic - starting with a critique of 'Africa Rising' and pursuing a series of case studies with particular reference to countries where 'elected dictators' have been trying to extend their terms of office and their real power - latest issue no. 10 is focused on Togo, where there has recently been a wave of popular protest. David Seddon